With a good deal of help from traditional media, the social media fad has grown into a worldwide phenomenon for millions who seem to have too much time on their hands. Many claim they use these sites to keep up with friends and relatives. But level-headed individuals use more direct means to keep up with loved ones. Many others are looking for love, or just an easy way to get sex, from whatever form it may come.

worldwide phenomenon for millions who seem to have too much time on their hands. Many claim they use these sites to keep up with friends and relatives. But level-headed individuals use more direct means to keep up with loved ones. Many others are looking for love, or just an easy way to get sex, from whatever form it may come.

Others claim to use these sites for “networking.” To those of you who insist these sites help advance your business or job prospects, I say this. Get up off of your ass and make something happen yourself instead of looking for easy ways to succeed, because success has no shortcuts.

The social media fad is not much different than its trash TV counterpart, which features episodes from the lives of dysfunctional individuals. Some are faced with the challenges of losing weight. Others are plain idiots who provide you with a look into their superficial, often pathetic and always trivial lives. Either way, many people have become fixated on the lives of others because they are unable to recognize the value in their own lives. I suppose for some, seeing how miserable others are makes one feel better about themselves.

When people aren’t glued to their TV sets watching the endless trash and censored media, many are engaged with their electronic devices. For many, a good part of that time is wasted on social media sites.

For a couple of years now, many have speculated about the timing of Facebook’s public offering. Over this

relatively short time span, the amount of press the company has received has been reminiscent of the dotcom days. As a part of this speculation, a couple of years ago Facebook was valued at around $5 billion. Back then, a few chumps even claimed it was worth $15 billion, despite the fact that they had no experience or training in valuation analysis. Last year Facebook was valued at anywhere from $12 to $20 billion, depending on which paid clown you asked. Today, the valuations typically exceed $20 billion.

There have been all kinds of metrics used to value Facebook; number of subscribers, subscriber growth, time spent on the site per subscriber per unit time, page views, average revenue per subscriber, and so on. Let’s have a look at one of the more commonly used valuation metrics; average revenue per subscriber. In 2010 Facebook generated an estimated $490 million in profits from total revenues of $1.5 billion (unofficial numbers). Based on these numbers, I can only see how a fool or crook might argue the company is worth $20 billion. What I would like see are the business risk and growth rate estimations.

You see, there are two types of valuations to consider. First, there’s the valuation based on what an individual would pay for a business. Let’s call this the buyer’s valuation. This valuation is usually much more credible because the buyer actually uses his own money, or else he must obtain financing from a bank. If the buyer is a savvy business man he is going to account for all risks involved before forking over this kind of money (if he intends on keeping the business long-term). If a commercial bank is involved in financing the deal, you can bet the bankers are going to go over every detail with a fine-toothed comb, looking for signs of risk.

Next, there’s the valuation based on how much the business owner can inflate the sales price. I will call this the seller’s valuation. Usually, when the buyer plans on keeping the business there is a back and forth struggle for final valuation between buyer and seller. But when the buyer is an investment bank the valuation is based largely on how much they think they can flip it to others for in a public offering. So in this later case the company only receives seller’s valuation because the buyers aren’t involved in the valuation process.

Thus, as you can imagine when Wall Street gets involved in the IPO game, many stocks collapse within a couple of years of their IPO price. Most venture capital firms play the same game, especially if their investment occurs towards the later stages because this means an IPO (which represents a means of exit) is more likely. In short, venture firms involved in late-stage financing deals act no different than Wall Street investment banking firms when it comes to inflated valuations.

In the past, I stated that Facebook was worth maybe a few hundred million dollars. However, this was a rough estimate not based on specific revenue and income data. Based on these latest estimates, I would value Facebook at no more than $1.5 billion, assuming I would even buy this questionable business.

Some of you might be thinking at that price Facebook would be a steal, right? After all, assuming things go reasonably well, the profits should be able to pay for the sales price plus financing costs within three years, or maybe four or five at if the company hits a few road bumps, right?

The problem is that this estimated return on investment has not accounted for some of the more critical types of risk involved, nor has it accounted for other important considerations, such as the value of Facebook’s assets, or rather lack thereof.

For instance, if I decided to buy a small chemical company, say a mini-Dow Chemical for $1.5 billion (forget that it is likely to have net debt) it wouldn’t face the risk of business failure anytime soon unless a catastrophic event occurred (like a Union Carbide-like disaster). While earnings would plummet after such an unlikely event, the fact is that the company would still retain a net worth due to its valuable asset base and intellectual property portfolio.

Thus, if I bought this chemical company I would be receiving tangible assets with a sizable value, in addition to any earnings these assets generated. As a result, I could sell off some of the business units and recoup at least part of my initial investment if the business was jeopardized. Moreover, the assets are tangible, so they are less risky because the depreciation and appreciation of these assets are more easily predicted. These are just a couple of important considerations that must be taken into account during the valuation process.

Facebook is an entirely different beast. It has very little intellectual property, or the intellectual property is not particularly valuable (despite what management may claim). And it certainly doesn’t have many tangible assets. In fact, the most valuable asset Facebook has is not only intangible, but it is not owned by the company. That asset is the key driver of Facebook’s success, and it could disappear in a relatively short time span. That asset is the buzz for Facebook. It’s been responsible for adding the vast majority of users.

As a result of the buzz, Facebook’s earnings are only based on the size and strength of its user base. But that could change at any time since the company does not offer any uniquely valuable goods or services. As a result, there is a great deal of risk involved in purchasing the company for anything more than $1.5 billion if the intent is to use it as a standalone business. If acquired by a large diversified firm, I would say the valuation could be considerably higher, but nowhere near say $8 billion.

It’s crucial to consider business risk and the size of the asset base when assessing valuation of a privately-held, relatively new firm within a relatively new sector. New companies face a great deal of business risk. And new companies within new industries face an even greater deal of risk. In addition, when estimating the valuation of Facebook, it's important to keep in mind that it has no real competitive advantage. Thus, the ability of competitors to steal market share presents a huge risk.

Websites like Amazon are much different because it has developed several competitive advantages. In addition, as an e-commerce company it sells tangible goods and services that are needed by consumers and businesses. Amazon has also created and acquired a good deal of assets, both tangible and intangible. Finally, Amazon is a well-established company and has demonstrated a proven ability to overcome numerous challenges through the brilliant leadership of Jeff Bezos.

Facebook is much different. Although the site has opened its door to allow app developers and encouraged content-sharing by users, advertising is likely to become the dominant driver of revenues in the future. The problem with this is that the traditional advertising model has proven to be relatively ineffective when transposed onto the Internet.

As Facebook continues to explore new ways of incorporating ads into its platform, it has introduced new terms of service resulting in widespread protest from many users. This in itself adds a good deal of risk, for if Facebook upsets a critical mass of users, it faces the risk of a cascade effect. Thus far, users have won nearly every case that they have protested, forcing Facebook to remove new changes to the Terms of Service and other changes to functionality that address privacy concerns.

Facebook continues to struggle to strike a balance between pleasing firms that shell out money for ads, and users who don’t want their information made public. As a part of this struggle, there has even been discussion (rumor) of a monthly user fee for use of the site, although I cannot confirm whether or not this came from management (unlikely). A subscriber-based revenue model would most likely sink the business quickly.

As more investment capital floods into the company, pressure will grow to generate more revenues. Thus, in absence of value-added applications the advertising side of the business will be placed at the center of focus. This means further intrusion of user information will be inevitable.

One of the most vulnerable aspects of social media is that it is fueled exclusively by buzz. When the buzz is strong, social media platforms can generate a huge amount of traffic. But when the buzz fades, the traffic can shrink rapidly. As a result, without valuable content and in-demand and valuable applications, social media firms face an all-or-none situation. Thus, Facebook faces the challenge of pleasing its users (or deceiving them) over its ad sponsors until it is able to bring real value to the table.

For anyone who expects long-term earnings growth from a social media website that offers primitive yet very expensive games and other useless applications, I have some beach front property in Dallas, Texas I’d like to sell you. In short, Facebook has a long way to go if it plans to continue the kind of growth that can justify a multibillion dollar valuation. Anyone who does not realize that doesn’t recall the ridiculous valuations given to hundreds of useless companies during the dotcom bubble.

Until management finds new ways to add valuable content, it will need to design better ways of balancing user satisfaction and privacy of personal information with ad effectiveness. Ultimately, all media companies should focus on providing valuable content. This is something the media has failed to recognize. Instead, the industry continues to focus on the volume of content, all while pleasing its ad sponsors. In the end, the audience receives useless, deceptive content. This is specifically why the media is facing numerous bankruptcies.

Moving forward, Facebook will be in a much better position to transition away from its current status as a novelty site because of the large amount of financing it has been able to attract. However, such a transition will not be easy. Just ask Yahoo! Although Yahoo! focused early on by providing free content, much of which had some value, today the company remains in a downward spiral. The content has become almost completely useless. Yahoo! is now geared towards ad sponsors rather than users, and the results show.

But none of these concerns matter much to the financiers of Facebook because they don’t plan to take a long-term stake in the firm. Rather, they plan to pump it up and dump it off to the pigeons. Thus, they have attached a sellers’ valuation to the company.

But none of these concerns matter much to the financiers of Facebook because they don’t plan to take a long-term stake in the firm. Rather, they plan to pump it up and dump it off to the pigeons. Thus, they have attached a sellers’ valuation to the company.

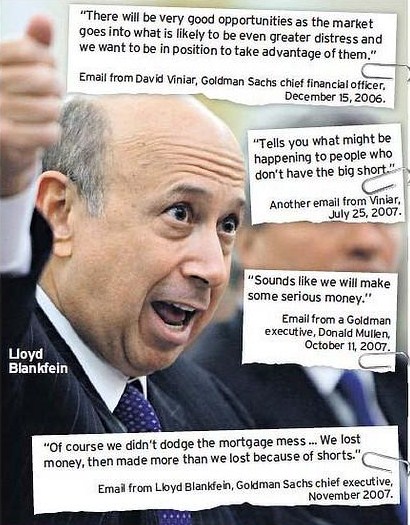

Goldman Sachs recently got its fangs around Facebook after providing the company with a $450 million investment stake. Goldman is now floating a $1.5 billion private placement memorandum to its clients to ensure the bank gets a great exit with no further risk. The deal terms value Facebook at an astonishing $50 billion.

This incredibly ridiculous valuation means that Facebook is worth more than Eli Lilly ($38.6 billion market cap), Bristol-Myers ($44.2 billion market cap), Unitedhealth ($42.2 billion market cap), Dow Chemical ($41 billion market cap), Dell Computers ($27.5 billion market cap), Research In Motion ($32 billion market cap), Starbucks ($24 billion market cap), and so on.

Certainly one cannot make a one-for-one comparison between Facebook and companies from other industries. But this very crude comparison gives you an idea how ridiculous Goldman’s valuation is. If you examine companies from a similar space, like Yahoo!, eBay and Amazon, they too are a good deal overvalued, especially Amazon. But at least they have been around for a while, they sell goods and services consumers want and often need, and they have come down from their dotcom bubble days.

industries. But this very crude comparison gives you an idea how ridiculous Goldman’s valuation is. If you examine companies from a similar space, like Yahoo!, eBay and Amazon, they too are a good deal overvalued, especially Amazon. But at least they have been around for a while, they sell goods and services consumers want and often need, and they have come down from their dotcom bubble days.

In order for Facebook to secure a long and profitable future, it must find ways to generate predictable revenue and income growth. As well, the valuation needs to come back down to earth. History tells us that Facebook’s valuation bubble is likely to burst only after it has exchanged hands from the venture industry and Wall Street, to Main Street.

A few years ago when the same buzz was being spread about Myspace, Rupert Murdoch shelled out nearly $600 million for the site. At the time, I stated this was a terrible purchase. But when you as desperate as Rupert Murdoch was, you will do many things.

At the time, Murdoch’s media empire was collapsing, not due to a bad economy, but due to the fact that more people have come to realize that the media serves the interests of corporations and Wall Street. Since Murdoch’s purchase of Myspace, things haven’t gotten much better for him, or any of the other media moguls for that matter. Meanwhile, Myspace continues to crumble, as reality sets in.

I would like to know if Murdoch would have paid out $600 million of his own money for Myspace. It’s easy to toss money around when it’s not coming from your own pocket. Yet, News Corporation shareholders sat around like fools and said nothing after the deal was announced. Many even celebrated the deal as a win.

This example illustrates why most people should never invest in securities. They don’t have an understanding of the valuation process, they don’t understand how venture firms or Wall Street banking departments work, and they aren’t able to get in when valuations are cheap. Instead they make the mistake of listening to the hype and propaganda delivered by Wall Street and its partner in crime, the financial media. This is how the game works.

This example illustrates why most people should never invest in securities. They don’t have an understanding of the valuation process, they don’t understand how venture firms or Wall Street banking departments work, and they aren’t able to get in when valuations are cheap. Instead they make the mistake of listening to the hype and propaganda delivered by Wall Street and its partner in crime, the financial media. This is how the game works.

Yet, after losing tremendous amounts of money when bubbles pop or other scams occur, most people keep coming back for more, hoping to strike it rich. Much of this mentality is created by the financial media and online brokerage commercials, which always deliver the message that it’s easy to make money in the stock market or that they can help you do well in the stock market by steering you to false epiphanies, like stock screening tools and research written by pinheads.

When Murdoch announced the intent of News Corporation to purchase MySpace, I was certain the buzz would wind down in a couple of years and be replaced by another social media website, and it was. As we look forward, it is likely that Facebook too will face a similar situation as MySpace with a few caveats.

When Murdoch announced the intent of News Corporation to purchase Myspace, I was certain the buzz would wind down in a couple of years and be replaced by another social media website, and it was. As we look forward, it is likely that Facebook too will face a similar situation as Myspace with a few caveats.

Due to its tremendous financing, Facebook will stick around a lot longer than Myspace. However, I can tell you this much with complete confidence. Facebook is being pumped up in order to dump it onto naïve investors. And it’s likely to lead to a disaster.

I consider what Goldman is doing to be securities fraud; another routine business deal for the firm.

![]()

![]()

Goldman’s investment in Facebook as well as its private placement to its clients also increases the likelihood that we will see a Facebook IPO over the next couple of years. The reason is simple. Goldman wants to secure a nice exit from its investment. And it’s using its own clients to secure a huge risk-free return.

The unfortunate reality is that once Facebook goes public, shareholders will be stuck with a ridiculously overvalued dotcom. While the publicly traded shares are likely to show some hysteria-like appreciation, it isn’t likely to last.

Based on my knowledge of the valuation process and understanding of how private shares are priced for public offerings, Goldman appears to be working with venture capital and Wall Street firms to pump up the valuation so they can dump shares onto naïve and greedy investors. These two characteristics almost always lead to a disastrous outcome. It’s time for the SEC to get involved before the thieves steal even more money using propaganda and their pull with the financial media to carry out this scam.

You aren’t likely to hear anyone else from Wall Street or the venture capital industry mention the Facebook![]()

![]() bubble.

bubble.

You are especially unlikely to hear industry professionals discuss the intent of Goldman to dump shares onto naïve investors because most of these guys are all the same.

If they are not directly involved with the scam, they certainly don’t want to expose what is going on because the pump-and-dump game is very common. And the next deal might involve them doing the same thing with another company.

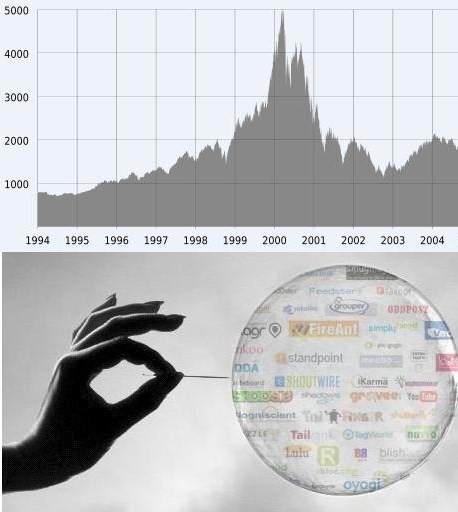

The last time a large scale pump-and-dump of this nature occurred was during the late 1990s. As we know, this led to the dotcom bubble. At the height of the bubble, Yahoo! had a market cap of more than $150 billion (compared to $22 billion today).

Murdoch’s deal with Myspace looked like a great buy when compared to some of the buyouts during the dotcom era, like @Home’s purchase of Excite for $8 billion, or Terra’s purchase of Lycos for $13 billion. You should note that Excite and Lycos are worth practically nothing today. This is likely to be the fate of Myspace down the road.

Thus, when viewed from the dotcom perspective, Goldman’s $50 billion valuation for Facebook might seem reasonable to those who believe that bubbles never burst.

The problem is that the worst time to buy is during the peak of a bubble. It appears as if Goldman is creating a bubble in social media. And by the time it pops, you can bet they will have exited with huge gains.

We see many similarities between the dotcom bubble and the most recent real estate-credit bubble. After hundreds of dotcoms and telecoms committed accounting and securities fraud resulting in trillions of dollars in losses to shareholders, not one single individual went to prison; not one company executive, not one Wall Street analyst.

We are seeing the same thing today, as not one Wall Street executive has been indicted for securities fraud that led to the global economic collapse.

Not one executive from credit rating agencies has been indicted, nor have any of the executives of Fannie Mae or Freddie Mac.

Goldman even struck a very sweet deal with the SEC to avoid criminal indictments by the Department of Justice. So if you think the SEC will stop Goldman from pumping and dumping Facebook, I wouldn’t hold my breath. The problem is that we have a fox guarding the hen house. This precisely why fraud has become synonymous with Wall Street.

Even without the assistance from the SEC and other financial regulators, Wall Street could not achieve much of its fraud without the help of others. The media is a principal partner in the game of Wall Street fraud. But individual investors are also key participants.

Without the greed and ignorance of Main Street, Wall Street would have a much more difficult time carrying out its fraudulent activities.

Although many investors might agree that Facebook has become extremely overvalued, they are likely to try to ride it all the way up and dump their shares before it comes tumbling down; if it were only so easy.

Once people realize social networking sites are really a new form of media disguised as free resources (i.e. social media) they just might recognize these sites are being dishonest because using them comes in exchange for something. That something generates money. And they aren’t about to tell you exactly how they plan to leverage your information and your personal habits, or what could be argued as tapping into your mind to generate revenues.

On a positive note for Facebook and all other social media, with each passing day more people are becoming naïve, lazy and stupid. So they are not likely to wake up to the fact that they are being exposed to more harm than benefit by use of these sites. Thus, another chapter is likely to be written in the book of Wall Street fraud and investor losses.

For those of you who aren’t familiar with me (due to the widespread ban I have faced by the media and virtually every website), I have been involved in both the public and private markets for a number of years, working with some of the largest and most highly regarded Wall Street and venture capital firms.

You might want to familiarize yourself with my track record and understanding of the valuation process before you write off this analysis.

Restrictions Against Reproduction: No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, scanning, or otherwise, except as permitted under Section 107 or 108 of the 1976 United States Copyright Act, without the prior written permission of the copyright owner and the Publisher.

These articles and commentaries cannot be reposted or used in any publications for which there is any revenue generated directly or indirectly. These articles cannot be used to enhance the viewer appeal of any website, including any ad revenue on the website, other than those sites for which specific written permission has been granted. Any such violations are unlawful and violators will be prosecuted in accordance with these laws.

Article 19 of the United Nations' Universal Declaration of Human Rights: Everyone has the right to freedom of opinion and expression; this right includes freedom to hold opinions without interference and to seek, receive and impart information and ideas through any media and regardless of frontiers.

This publication (written, audio and video) represents the commentary and/or criticisms from Mike Stathis or other individuals affiliated with Mike Stathis or AVA Investment Analytics (referred to hereafter as the “author”). Therefore, the commentary and/or criticisms only serve as an opinion and therefore should not be taken to be factual representations, regardless of what might be stated in these commentaries/criticisms. There is always a possibility that the author has made one or more unintentional errors, misspoke, misinterpreted information, and/or excluded information which might have altered the commentary and/or criticisms. Hence, you are advised to conduct your own independent investigations so that you can form your own conclusions. We encourage the public to contact us if we have made any errors in statements or assumptions. We also encourage the public to contact us if we have left out relevant information which might alter our conclusions. We cannot promise a response, but we will consider all valid information.

Please listen to this video (especially if you are Jewish) in order to understand our viewpoint. ...

The Facebook pump-and-dump scam has played out just as I predicted. After only a couple of months, naive shareholders who feel for this scam have already lost nearly $45 billion as the result of a col...

For background info see The Solution to Greece's Sovereign Debt Crisis After suffering through nearly five years of a very severe recession, the worst is yet to come for the Greek people. Acc...

In the past, I have written some pieces on Obama, Alex Jones and Ron Paul. Because I cover so many things, from investment and economic analysis, to healthcare and politics, my time continues to beco...

Previously I discussed the dangers of the media, pointing to numerous examples, from Google and Yahoo! to Wikipedia. I also discussed how Wall Street and venture firms orchestrate pump-and-dump scheme...

Previously I discussed the dangers of the media, pointing to numerous examples, from Google and Yahoo! to Wikipedia. I also discussed how Wall Street and venture firms orchestrate pump-and-dump scheme...

Careful observers can spot numerous examples of Jewish control, fraud and deceit everywhere they look. These deviant activities are widespread throughout Wall Street, the banking industry, the med...

We continue from Part 1 Facebook’s Bait-and-Switch When Facebook began it didn’t have any advertisements. Similar to most small companies which embrace the capitalist growth mode...

In many ways, the social media craze really isn’t much different than its trash TV counterpart, which often features episodes from the lives of self-absorbed, dysfunctional, attention-seeking in...

To give you an idea of the type of scum aligned with the globalist push to enslave people through further corporatization and policies which empower banks, all while robbing citizens of prom...

While still working on Wall Street, I began recommending gold in late 2001 to my clients just when the bull market had commenced. As you might imagine, it was very difficult to convince older investor...

With a good deal of help from traditional media, the social media fad has grown into a worldwide phenomenon for millions who seem to have too much time on their hands. Many claim they use these s...

Over the past few months we have heard about a variety of questionable practices from banks looking to seize the homes due to chronic mortgage delinquencies. Each day more drama is added to the pictur...

Mike has been targeted by WikiLeaks because of his highly successful proprietary trading methodologies which have successfully predicted and timed the stock market collapse down to a few hundred point...

I wanted to show you an everyday example of the dangers of Yahoo! But you should note that this example applies to all websites. Below is a recent article featured on Yahoo!'s homepage disc...