Stay Clear of Traditional Asset Classes

Washington continues to manipulate economic data, as it has for several years. The past few Establishment Survey reports confirm the deception of data, as many more jobs were lost than official numbers indicate.

A better gauge of economic weakness, in my opinion, is consumer and mortgage late-payment and default rates, since this data is more difficult to manipulate. This is especially true for late credit card payments.

Washington continues this deception in order to extend the illusion of economic growth. It keeps consumer confidence high, promising excess consumption. Asia and Europe are happy to finance America’s debt because this keeps interest rates low in the U.S., which provides consumers with inexpensive credit to spend more of what they don’t have, mainly on imports.

Think about it. When money is tight, households struggle just to get by. Most families end up spending so much on gas, food, healthcare and schooling that they don’t have much left over for that LCD widescreen, a new computer, or a fuel-efficient car; you know – the stuff that comes from Asia and Europe. Foreign economies feel the effects when U.S. consumers aren’t spending.

A weak economy also hurts U.S. companies. In response, they cut expenses by lowering employee benefits and sending jobs overseas. The low labor costs provides consumers with less expensive electronics, automobiles, textiles, furniture and many other items, most of which are now made overseas.

Asia and Europe finance Washington’s wasteful spending because it keeps interest rates low, which makes credit inexpensive. So consumers have access to inexpensive credit which allows them to buy that BMW or plasma TV, Washington has money to waste in Iraq, and foreigners experience improved living standards via jobs created by U.S. companies.

But hasn’t this helped U.S. consumers?

After all, Americans can now buy a nice laptop for $400.

Who cares? What matters is that they’re paying ridiculous prices for basic necessities – gasoline, food, education, and healthcare. Washington needs to rethink its economic policies. Americans should be empowered as workers first and consumers second. Only in this way will America be able sustain economic productivity.

Instead, U.S. corporations and foreign workers are benefiting at the expense of working-class Americans, who continue to lose jobs due to outsourcing. If they’re lucky, displaced workers are now underemployed, working for much less and for no benefits at jobs that fail to utilize their talents and experience.

Others become the forgotten – discouraged workers, who can’t find work and are no longer counted in unemployment data. For working-class Americans, this ridiculous economic policy resembles a pyramid scheme. For the wealthy elite, large corporations, and foreign nations, it’s a gravy train.

No longer can Washington hide the painful correction that lies ahead. We are now seeing the early stages of what promises be the worst recession in decades. Yet, this is only a prelude of what to expect over the next several years. Washington’s ability and commitment to manipulate data will lead to further periods of economic deception.

But just as was accomplished in the 2004-2006 period by Alan “Bubblespan,” the consequences will be harsh thereafter. Throughout this challenging period, investors would be wise to consider realignment of their investment portfolios to reflect macroeconomic trends – precious metals, commodities, energy, TIPS, and foreign currencies.

I find it remarkable how so many continue to deny the problems in the economy. Just look at the data on foreclosures, home price declines, new and existing home sales, new housing permits, and consumer debt defaults.

Even with a banking system bailout by the Fed of over $1 trillion of taxpayer funds (with more to come) the credit crisis continues to worsen. This was not difficult to predict in advance if one had bothered to analyze the data. Yet, many still underestimate the consequences of a bubble economy that’s run out of air. Soon, consumers will fall flat on their face.

No amount of credit will ease the pain of record debt, the falling dollar, and soaring inflation. In fact, it will only worsen the blow. Bernanke is adding gasoline to the fire. Very few jobs have been created under President Bush, other than military, government-related positions and jobs with little or no benefits. Yet, all of these jobs contribute to official employment numbers.

Much of the private sector jobs created over the past few years came about via courtesy of Alan Greenspan’s real estate bubble – real estate agents, loan officers, mortgage bankers, construction, appraisers, etc. Needless to say, a good portion of these jobs no longer exist. And many more will disappear over the next two years.

Instead of wage and job growth – the typical elements of economic recoveries – the economy has been fueled primarily with cash-out financings since 2003. And now reality is setting in. Since 2004, Wall Street chose to focus on corporate profits. A four-year period of record profits caused the market to soar in 2007. But these gains were achieved by the cost advantages of outsourcing, excessive credit spending by consumers who used their homes as ATM machines, and inexpensive goods supplied by China (due to currency manipulation).

Thus, corporate America thrived while sending jobs overseas, adding to economic expansions in Asia, Europe, and Latin America. And this was enough to send the stock market well beyond previous highs. A year ago, most investors also focused only on corporate profits because that was the approach Wall Street took.

They did not consider the impact of many years of record deficits, wasteful spending in Iraq, record oil prices, rising inflation, muted real wage growth, and the declining dollar. Instead, they chose to believe the data from Washington without question – impressive unemployment, GDP, and inflation data. Despite record profits, even healthy companies froze pension plans and cut employee benefits because they can.

Shareholder value is all that matters to America’s corporations. American workers are now treated as commodities that can be replaced by less costly alternatives from Asia. But now, inflation coupled with massive job losses and frozen wages have added to the real estate fallout. How can Washington, Wall Street, and the media continue to deny the truth?

Now the Federal Reserve has come to the rescue – not to help consumers, but banks – passing out billions in U.S. Treasuries to the mega-banks in exchange for junk bonds. This has devalued the dollar further, which has led to higher oil prices, which has contributed significantly to massive inflation in food prices.

With continued devaluation of the dollar, there is no doubt this will be the worst recession in decades. As I predicted in 2006, we are now seeing the corrective effects of an economy propped up by the largest real estate bubble in U.S. history. And it’s only going to get worse.

Commercial mortgages have already started to weaken. As the economy weakens further, millions of prime mortgages could default. The non-borrowed banking reserves are negative. This means the U.S. banking system would be insolvent without the help of the Fed's printing presses. Yet, even with so much cash from the Fed, most banks are still struggling to unwind the 20-30:1 leverage built upon mortgage-related debt, most of which is junk.

The real inflation rate is already above 10%, despite Washington's official numbers, which it continues to twist using hedonics. If inflation is not a huge problem, why did the Fed stop reporting M3 last year, just when it hit a 33-year high? Why did Washington pull the Economic Indicators website on March 1, 2008? The excuse given was due to "budgetary constraints" which makes it even more obvious Washington is trying to avoid an all-out panic.

Greenspan caused this crisis, and Bernanke is finishing the job. While the EU central bank continues to emphasize monetary policies focused on inflation control to protect consumers, the Federal Reserve remains committed to the best interests of Wall Street and the banks, while U.S. consumers struggle with gas and food prices. It appears as if the Fed is willing to destroy the financial stability of consumers in order to protect the reckless and greedy behavior of the banks.

But the Fed cannot keep running away from the mistakes it has made. Applying band aids to holes in the Hoover Dam will only delay what will be a much more severe crisis at a later point. Greenspan used the same strategy after the Internet meltdown. And of course this resulted in the real estate bubble, which promises to create much harsher consequences.

At this juncture Bernanke really doesn’t have much of a choice because he let things deteriorate too far before reacting. It’s difficult to imagine that he didn’t see what was happening a year earlier. If he truly didn’t, he should resign and state incompetence as his reason. It’s almost as if he intentionally ignored the obvious and waited for a crisis so he could justify destroying the dollar through excessive inflation.

Why would Bernanke want to decimate the dollar even further? Given the unfair free trade policies of Washington, it looks as if the only solution to the record trade deficit is to wipe out the dollar. That might be the only way to regenerate domestic manufacturing. But this logic is flawed. No nation can have a good economy when its currency is weak. We already see how a weak dollar affects oil prices.

What purpose might inflation have? Well, for one, it would help Washington to pay off its massive debt. As well, GDP data would be boosted, creating the illusion of a recovery. America has consumed 6% more than it produced for over a decade. And it has relied on Asia and Europe to finance its spending spree. Clearly, the cumulative effects of this disparity have begun to correct.

The first attempt at payback was the Internet meltdown. But Greenspan insisted on stopping a full correction. As a result, we now see a much bigger payback – the real estate and banking crisis. Continuing in the tradition of Greenspan, Ben Bernanke won’t allow a full correction. The economy needs to feel the full pain of this bubble correction. This means no bank bailouts, stop the printing presses, and provide real help to consumers instead of a $600 gift certificate to Best Buy (BBY).

Washington needs to restructure free trade so that all nations are on a level playing field, provide tax incentives for corporations that create domestic manufacturing facilities. Thereafter, the economy would be positioned to start anew, with no further surprises down the road. Of course this won’t happen as long as lobbyists continue to buy off politicians.

Government bailouts create a moral hazard by rewarding irresponsibility at the expense of taxpayers. Ultimately, this ridiculous policy by the Fed reinforces the monopolistic characteristics seen in many of America’s industries, promising further devastation for consumers down the road. The boom-and-bust cycles created by the Fed’s reckless monetary policies ensures the continued decline of the U.S. Washington needs to understand that America’s excess consumption trends are becoming less advantageous to its Asian and European creditors since consumers have no more money to buy their goods.

In contrast, Asian and European consumers have double-digit savings rates. Soon, much of corporate America will relocate entire operations overseas, not only for labor cost advantages, but to serve what will soon represent its best consumers – three billion Asians with healthy household savings. This is certain to eliminate America’s edge in innovation due to the inevitable transfer of intellectual property seen under free trade economics. Finally, without the reckless spending of U.S. consumers, foreign nations will no longer have reason to hold U.S. Treasuries.

Already, every nation wants out of the dollar because they understand the worst is yet to come. In the next few years, there will most likely be a brief period whereby consumers think the worst is over. But this illusion will be due to the trickery of the Federal Reserve and Washington.

There is no way to avert the payback period that has been building for over two decades. And the entry of 80 million baby boomers into entitlement programs promises to push America deeper into a depression. It would be extraordinarily difficult to find a way out of this mess. Even expected benefit cuts for Medicare won’t help, as long as the healthcare industry is free to set prices as they chose.

In the best of scenarios, higher taxes and fewer medical benefits will force millions of boomers to spend what little they have on healthcare, with the rest going to food and utilities. Imagine what that will do to consumer spending.

By 2009, I expect corporate bankruptcies to soar, including several bank failures, perhaps hundreds. Already, the FDIC is beefing up its staff in anticipation of a more severe banking collapse. Most consumers won’t think much of it when these smaller banks fail because, rather than close their doors, the mega-banks with buy them using the printing presses of the Fed.

A few months ago, banks began the painful process of trying to write down bad mortgage debt. But mortgage defaults continued to pile up. So they had to keep writing down the debt more and more, until finally, much of it became virtually worthless.

In order to avoid a liquidity crisis, banks were forced to sell off their highest quality debt, causing more damage to the balance sheet. After the run on Bear Stearns (BSC), the Fed realized that any bank could become insolvent overnight. And that would cause a snowball effect. Therefore, Bernanke extended emergency funding options (once previously reserved for commercial banks) to investment banks – something not done since the Great Depression.

Now the Fed has increased reserves to $150 billion for May alone. Combined with another rate cut last week, the dollar will continue its downward spiral. Bernanke’s commitment to inflation will vaporize retirement savings in a few years unless radical changes are made.

Bank write downs will persist throughout the year and continue through at least 2009. Even that optimistic scenario won’t signal a buy for investors. It’s likely that many years will pass before the banking system recovers from this mess. Before it’s all said and done, most banks will face a huge dilution in earnings after issuing millions of new shares to private equity, LBO and sovereign funds.

In the meantime, there will be excellent trading opportunities if one has a strong stomach. Prior to its recent financing by TPG, I viewed Washington Mutual (WM) as the bank most at risk of insolvency. With over $7 billion of new cash, I still feel it will need a lot more cash or a lot of luck to remain solvent.

Even Citigroup (C) isn’t out of the woods. Until it eliminates its dividend, I would not consider entering as a long-term investor. Keeping the dividend shows that management underestimates the problems.

Already, the Federal Reserve has pumped over $1 trillion into the banking system. Combined with the European Central Bank, over $1.5 trillion has been lent to banks in an attempt to restore liquidity.

In my estimates, an additional $1.5 to $2 trillion will be needed for absolute liquidity (barring a credit default swaps meltdown). If these estimates turn out to be correct, the dollar will collapse from current levels. Likewise, the real estate correction will most definitely persist for several years. But there will be select regions that will rebound much sooner.

Throughout this period, oil prices will climb higher, as will commodities and inflation. Finally, interest rates will soar. All of this could combine to keep real estate prices contained for several years.

I stand by my 2006 estimates for the real estate meltdown, with a 30% to 35% decline in real estate from peak levels across the nation. Thus far, there has been about a 15-18% decline from the peak. Other estimates I made in 2006 predict a 1-3% annualized return from the Dow during the current bear market period (the period beginning in 2001 and persisting through 2012). Thus far, this has held firmly in place. On an annualized basis, the Dow is up by about 1.5% since 2001. Furthermore, if you adjust the price of the Dow to account for the declining dollar, it stands at around 8500.

In total, the effects of the real estate and banking crisis will most likely cause total losses of over $10 trillion. Even without a global meltdown of the financial system, U.S. banks will end up losing up to $1 trillion–about six times the losses from the Savings and Loan crisis in 1988. Homeowners will lose about $6 trillion on paper from the value of their homes. And job losses due to the real estate and banking crisis will account for the remainder. Municipalities are already feeling the squeeze due to declining home values and record foreclosures.

Over the next two years, most cities will face huge budget deficits due to diminished sales and property tax revenues. California has already declared a state of fiscal emergency due to an estimated $20 billion budget deficit expected over the next 15 months.

Still, all of this may be minor compared to the increasing risk of a meltdown in the $40 trillion credit default swaps market. While some feel that a temporary decline in home values will not cause any damage to them, consider that the normal rate of home sales due to job changes, divorces, death, etc. will cause a substantial percentage of this devaluation to be transformed into real losses.

As well, the wealth effect that was created during the bubble has now flip-flopped into the poor effect. Even homeowners with no outstanding mortgage debt will feel the pain of collapsing home values. And this alone will crush consumer spending. Plummeting home values have already caused many to walk away rather than honor their mortgage obligation. Can you blame them?

Despite all of the obvious signs, Washington and Wall Street remain in denial, as do the puppet TV and radio journalists. While many are clueless, the others see what’s going on. But they don’t want to reveal the truth because they’re afraid it will create a self-fulfilling prophecy.

Sorry, it’s too late. Consumers already expect the worst. Accordingly, consumer confidence recently hit a 26-year low. Despite reports from much of Wall Street that the worst is over, there will be much more devastation in the coming years.

Even after the real estate and banking problems subside, the problems for consumers will only get worse. The average American will struggle to pay for food, energy and healthcare. Rather than the 33% peak unemployment rate seen during the depression, America will have 50-60% underemployment rate. Inflation for basic necessities will persist for many years.

Americans don’t need less expensive electronics. They need affordable prices for basic necessities – gasoline, food, and healthcare. Doesn’t it seem odd that the things Americans need most are experiencing a hyperinflation trend? When America’s inflation crisis began in the ‘70s, oil surged, gold skyrocketed and the economy was faced with a brutalizing transition. Back then, it was in much better position to weather the storm because it was the world’s leading creditor. It was also more self-sufficient in producing its oil needs.

Today, America is the world’s largest debtor, while relying on foreign nations for most of its oil demand. Even if peak oil proves to be a myth, continued conflicts in the Middle East combined with soaring oil demand from Asia promises to move oil prices higher in the coming years.

With rare exception, investors should stay clear of traditional asset classes. If you haven’t already done so, you’d be wise to invest in commodities, gold, oil trusts, and foreign currencies (Yen and Swiss Franc). In addition, investors without short investment horizons should have some exposure in China and Latin America. Keeping cash on hand is also advised.

When the market sells off, you may choose to buy in. But don’t expect it to last. Buying the U.S. market after sell offs and moving to cash after rebounds is the best way to navigate this storm. A buy-and-hold strategy will crush most investors. Once rates begin to soar, Washington will no longer be able to suppress inflation data. At that point TIPS will be a good investment.

Over the next decade, I expect gold, select foreign currencies, oil trusts, TIPS, Chinese and Latin American equities to significantly outperform the U.S. stock market. Watch out though, because if things get really bad, the entire world will be affected. But that will represent a buying opportunity in Chinese and Brazilian equities.

The only exception I would make for traditional U.S. equities would be an investment in select drug makers (Pfizer (PFE), Bristol Myers Squibb (BMY), GlaxoSmithKline (GSK) and Merck (MRK) for investors with long investment horizons. Sure, each one has its fair share of problems to contend with, namely pipeline issues. But they still represent America’s only legal monopoly via drug patents. And Medicare Part D promises to boost profits for many years to come.

Currently, the market is way overbought, both for the short and intermediate-term. At this point, it has much more downside than upside so you should consider taking some money off the table. You might want to initiate or add small positions in gold streetTracks Gold ETF (GLD), Northgate Minerals Corporation (NXG) and oil trusts (Pengrowth Energy Trust (PGH), Penn West Energy (PWE) and Permian Basin Royalty Trust (PBT) due to recent corrections.

Finally, I would advise investors to consider taking some type of short position in financials pretty soon, preferably with an ETF, such as UltraShort Financials ProShares (SKF).

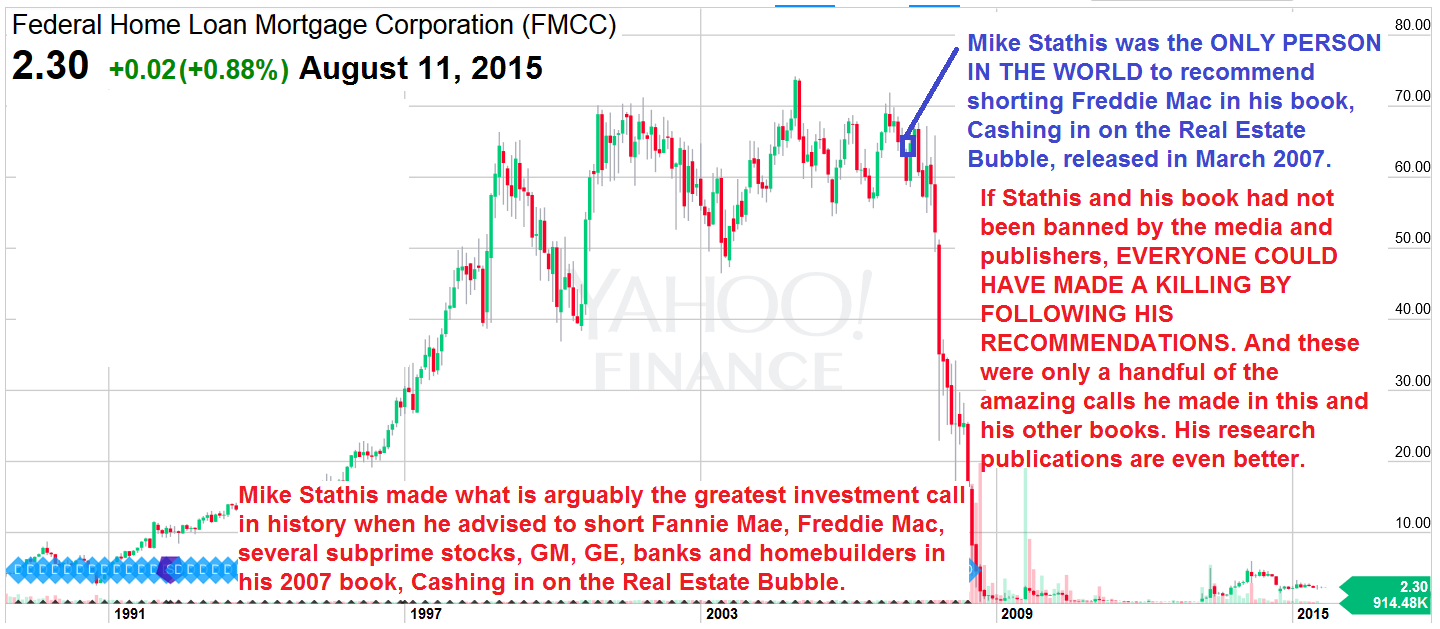

NOTE: Mike Stathis predicted the precise details of the financial crisis in his 2006 book, America's Financial Apocalypse.

The Jewish Mafia REFUSED to publish this landmark book because it exposed the widespread fraud committed by the Jewish Mafia.

Instead, the Jewish Mafia published useless marketing books written by their broken clock tribesmen (like Peter Schiff's useless book which was wrong about most things and was written a year AFTER Stathis' book).

Stathis also released a book focusing on strategies to profit from the real estate collapse in early 2007.

The Jewish media crime bosses prefer to simply ignore those who speak the truth and threaten to expose them as the best way to hide the scams from the public.

In contrast, the Jewish media crime bosses continuously promote Jewish con men and clowns who have terrible track records as a way to enrich them all while steering the audience to their sponsors, most of which are Jewish Wall Street and related firms. Figure it out folks. It's not rocket science.

__________________________________________________________________________________________________________________

Mike Stathis holds the best investment forecasting track record in the world since 2006.

Check here to download Chapter 12 of Cashing in on the Real Estate Bubble.

So why does the media continue to BAN Stathis?

Why does the media constantly air con men who have lousy track records?

These are critical questions to be answered.

You need to confront the media with these questions.

Watch the following videos and you will learn the answer to these questions:

You Will Lose Your Ass If You Listen To The Media

.png)

.jpg)

.png)

.png)

.png)

.png)